In a recent article, we discussed the ins and outs of mortgage points (or discount points) and whether or not it makes sense to pay them to decrease the interest rate on your mortgage.

As interest rates continue to rise, these “buydowns” are becoming more of a topic of conversation among home buyers and sellers, and their agents and lenders.

For those buyers who were on the cusp of qualifying for a mortgage to begin with, rising rates could spell disaster and prevent them from obtaining the amount of financing needed to buy a home.

This can also become a problem for sellers. According to a recent article by Mortgage News Daily, mortgage loan applications just hit their lowest levels in 22 years.

Even though we are still technically in a “seller’s market” (more demand for homes than supply), the tides are changing. Fewer buyers able to qualify for mortgage financing means fewer buyers bidding on homes. For those who are in a hurry to sell, this could mean having to reduce the price of the home to attract qualified buyers.

Neither buyers nor sellers win when interest rates go up like we are seeing today. However, there is a way for your mortgage and real estate team to work together to create a Win/Win scenario for everyone involved – the Seller-Paid Rate Buydown.

What Is A Seller-Paid Rate Buydown?

Lenders allow the seller of a home to “credit” a portion of their proceeds to the home buyer. This is called a seller concession. Seller concessions can be used to pay a buyer’s closing costs only, and cannot be used to help with the down payment.

What experienced mortgage and real estate professionals know is that seller concessions can also be used to pay mortgage points and buy down the interest rate.

The whole idea for the seller-paid rate buydown is to get money back from the seller to permanently buy down the interest rate. The majority of agents and mortgage professionals will distribute the seller funds to underwriting costs, escrow fees, and loan fees…not many of them think to permanently buy down the interest rate on the loan which significantly reduces the monthly mortgage payment.

Who Benefits From A Seller-Paid Rate Buydown?

At first thought, it may seem like a seller-paid rate buydown only benefits the buyer and not the seller.

In a typical seller’s market, where there are always multiple offers on homes and biddings wars are the norm, this may be true. But as we mentioned above, rising interest rates are throttling affordability and leading to fewer mortgage applications – especially for higher-priced homes.

When this is the case, the go-to solution is for the seller to reduce the asking price of the home. But this is actually not the best way to go. A seller-paid rate buydown will actually result in more profit for both the buyer AND the seller.

Let’s take a look at how that’s possible.

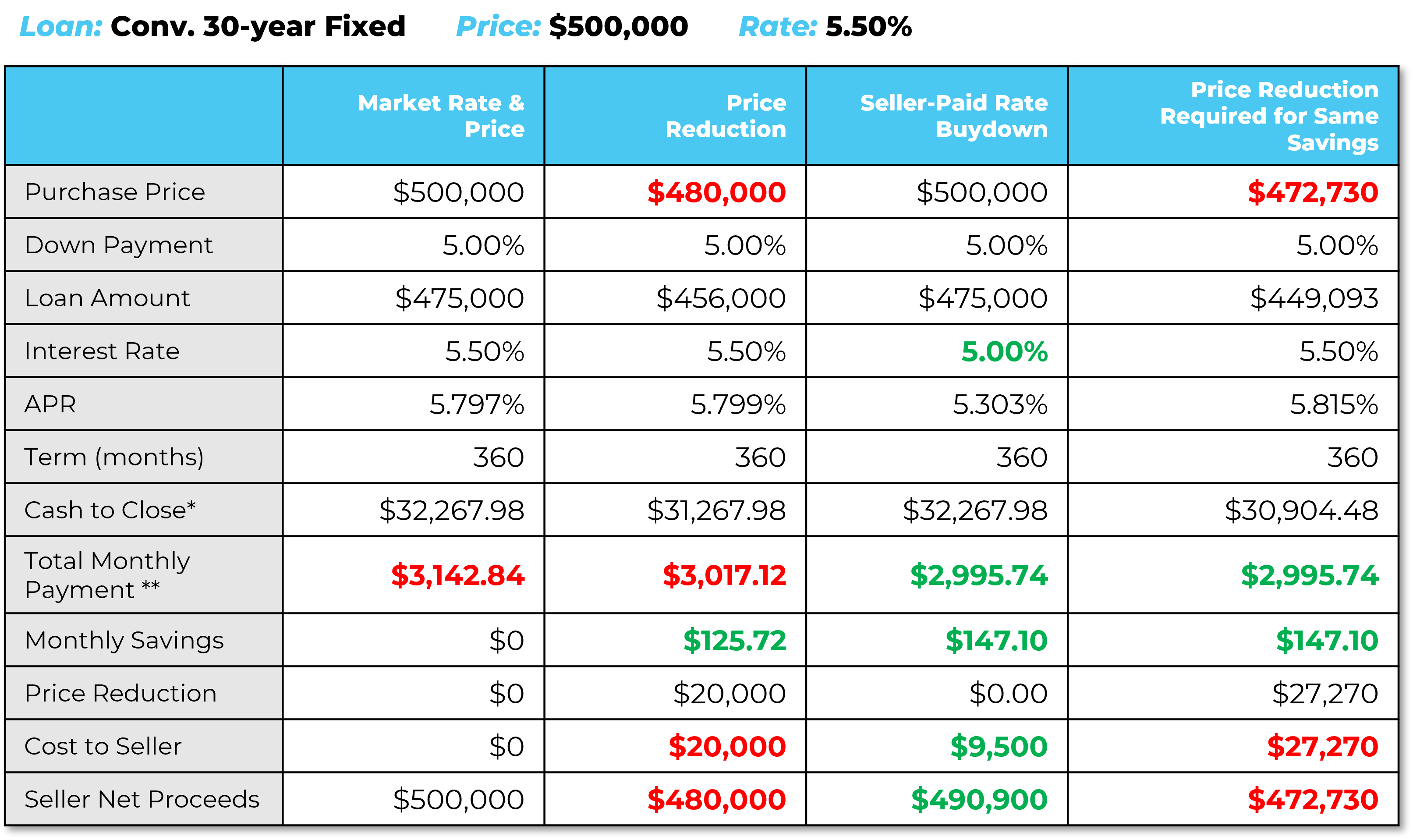

Below is a sample of a loan comparison showing options for purchasing a $500,000 home using a 30-year fixed-rate mortgage at a 5.5% interest rate.

For this example, let’s say the buyer is only able to qualify for a monthly payment of $3,000. As you can see in the first column showing the market rate and price, the buyer would not be able to afford the home in this scenario.

Price Reduction Strategy

Take a look at how this would change if the seller reduced the price of the home by $20,000.

This change would result in some savings for the buyer, but the required monthly payment would still be too high. This strategy would also reduce the seller’s net profit by $20,000 – a considerable amount.

Seller-Paid Rate Buydown Strategy

Now look at what would happen if the seller paid 2 points to buy down the interest rate by .5%.

Not only would this option reduce the monthly payment enough to what the buyer could qualify for, it would also increase the seller’s net profit by $10,500 compared to the price reduction strategy.

To take it a step further, the final column shows how much the seller would actually have to reduce the price of the home to reach the same monthly payment as the rate buydown strategy – $27,270, which is nearly 3 times the cost!

And finally, by reducing the interest rate, the buyer will realize more savings over the life of their loan – not just upfront.

The Bottom Line

Negotiations about price and seller concessions are part of every real estate transaction. What many do not realize is that a seller-paid rate buydown strategy offers more benefits for all parties involved in the long run:

- Offering a below-market interest rate for the property will entice more buyers

- Saves the seller money upfront

- Saves the buyer money in the long run with lower payments and a lower interest rate

- Helps hold home values for the area

- Avoids the stigma of a price reduction

If you would like to learn more about the benefits of a seller-paid rate buydown strategy, or if you would like to see a loan comparison similar to the one above for your particular purchase scenario, fill out the form below to request a mortgage discovery consultation with one of our experienced mortgage advisors.